Down Payment Assistance Programs Your Homebuying Guide

- Sep 15, 2025

- 15 min read

So, what exactly is down payment assistance? Think of it as a helping hand that bridges the gap between what you’ve saved and what you need upfront to buy a home. These programs provide funds, often as grants or special loans, to cover your down payment and closing costs.

This support is a game-changer for so many people who can comfortably handle monthly mortgage payments but find it tough to pull together the large lump sum needed at closing.

How Down Payment Assistance Unlocks Homeownership

For a lot of hopeful homebuyers, the biggest hurdle isn't the monthly mortgage payment—it's saving up for that initial down payment. With home prices on the rise, coming up with 10% to 20% in cash can feel like a mountain too high to climb. That’s exactly where down payment assistance programs (DPA) come in.

These programs aren’t just one-size-fits-all. They're a whole collection of different financial tools designed to make homeownership more attainable. You’ll find them sponsored by all sorts of organizations, including federal, state, and local government agencies, as well as non-profits and even some employers.

A Growing Network of Support

The world of homebuyer aid is getting bigger and better all the time. In fact, there's never been more help available. As of early 2025, there were 2,509 homebuyer assistance programs active across the United States, offering an average benefit of around $18,000. That's the highest number ever recorded, which shows a real commitment to creating more paths to owning a home.

The goal of these programs is simple: help qualified buyers get past the biggest financial barrier to homeownership. They exist because many people have the steady income for a mortgage but just don't have the massive savings needed for the initial investment.

DPA can drastically cut the amount of cash you need to bring to the closing table, letting you buy a home much sooner than you might have imagined. It also means you can hold onto your personal savings for other important things, like moving expenses, new furniture, or just a healthy emergency fund.

To get a clearer picture of the entire homebuying journey, take a look at our guide on the steps to buying your first home. By making that initial purchase more manageable, these programs empower individuals and families to start building equity and long-term financial stability.

Understanding Your Down Payment Assistance Options

Dipping your toes into the world of down payment assistance programs can feel a little overwhelming at first. There's a lot of new terminology, and each program offers a different flavor of support, designed for specific financial situations.

Think of it like choosing the right tool for a home improvement project—you wouldn't grab a hammer when you really need a screwdriver. The best type of assistance depends entirely on your long-term goals, your current financial picture, and how you feel about managing debt down the road. Getting a handle on these differences is the first real step to finding the right support.

Before you dive in, it’s a good idea to get a baseline. You can calculate your potential down payment to get a rough idea of what you might need for homes in your price range.

Grants: The Gift of Equity

The most straightforward—and let's be honest, the most exciting—form of help is a grant. A grant is exactly what it sounds like: gift money. It’s a sum of money given to you by a qualifying organization that you never, ever have to pay back.

This is pretty much the holy grail of down payment assistance. It comes with no repayment strings attached, giving you an immediate boost to your home equity without adding a single penny of future debt. For buyers who meet the criteria, it's a massive leg up.

Forgivable Loans: The Disappearing Debt

Next, you have forgivable loans, which are a cool hybrid between a gift and a traditional loan. These are usually set up as "silent second mortgages," which is a fancy way of saying you get the money upfront but don't have to make monthly payments on it.

The real magic is in the forgiveness clause. Typically, the loan is forgiven over a set period—say, 20% each year for five years—as long as you continue to own and live in the home. If you stay put for the entire term, the debt just vanishes. But, if you sell, move, or refinance before that time is up, you'll likely have to pay back a prorated amount.

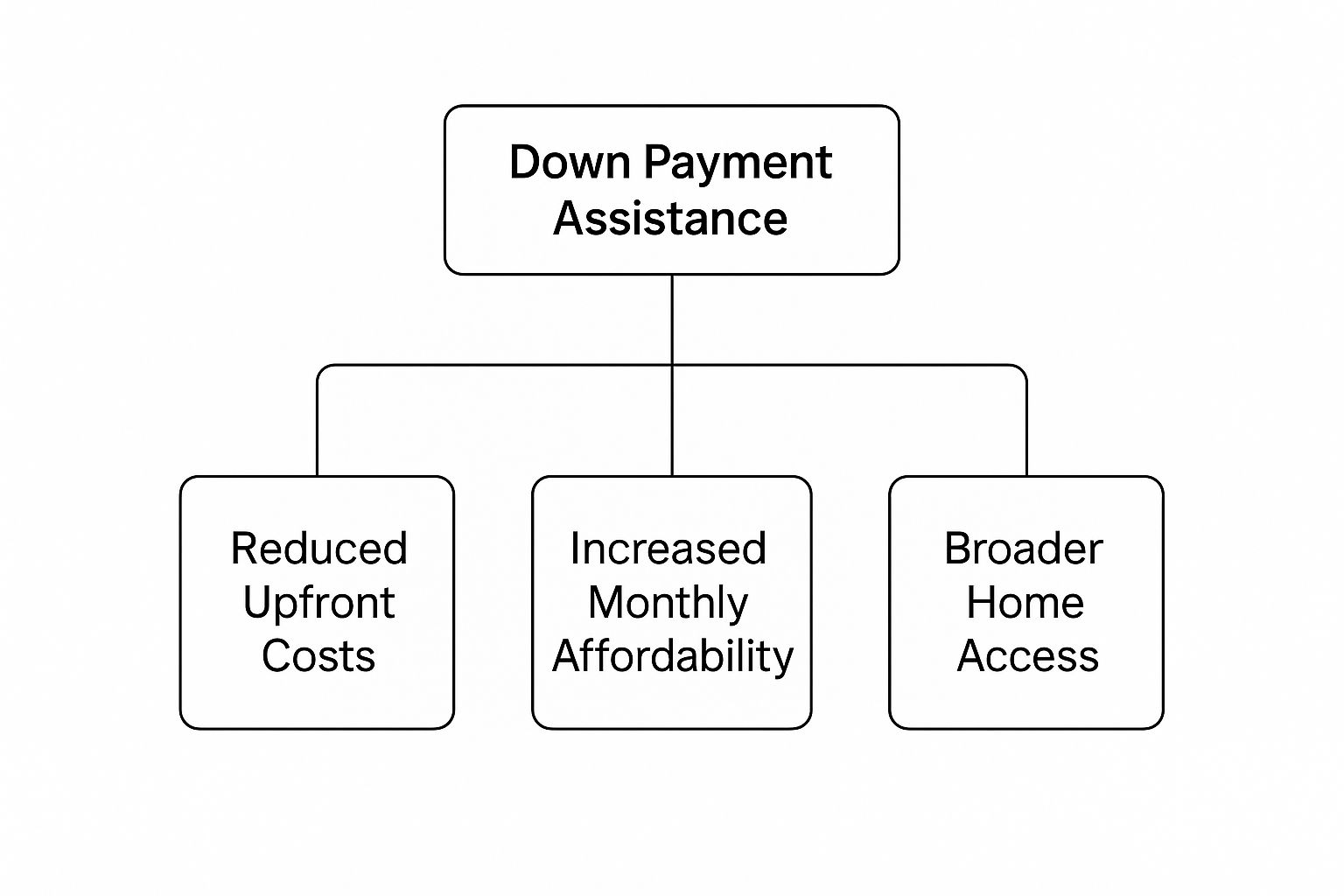

This infographic breaks down how these assistance types directly translate into real homeownership benefits.

As you can see, the whole point of DPA is to knock down that initial financial wall, making homeownership a real possibility for more people and improving long-term affordability.

Deferred Payment Loans: The Pay-It-Later Plan

A deferred payment loan is another popular route that lets you postpone repayment. Just like a forgivable loan, it’s a second mortgage with no monthly payments eating into your budget.

The big difference is that the debt isn't forgiven over time. Instead, the full loan amount becomes due when a specific "trigger event" happens. This is usually one of three things:

You sell the home: The loan gets paid back from the sale proceeds.

You refinance your main mortgage: You'll typically pay off the DPA loan during the refi process.

You pay off your main mortgage: Once your primary home loan is settled, the DPA loan comes due.

These are a fantastic choice for buyers who need a hand now but expect to be in a much stronger financial spot in the future.

Low-Interest Loans: A Helping Hand with Repayment

Finally, some programs offer low-interest repayable loans. These work just like a standard second mortgage: you borrow the funds for your down payment and then pay it back through regular monthly installments.

While this does add a little bit to your total monthly housing cost, the terms are almost always incredibly generous. The interest rates are usually way below market—sometimes even 0%—and the repayment period is often stretched out over 10 years or more to keep the payments manageable.

Key Takeaway: The type of down payment assistance you choose will directly impact your finances for years to come. Whether it’s a no-strings-attached grant or a structured loan, each option is designed to make homeownership a reality for those struggling to save for the initial costs.

To help you see the differences more clearly, let's put these options side-by-side.

Comparing Down Payment Assistance Program Types

This table breaks down the key features of the most common types of down payment assistance to help you decide which is right for you.

Assistance Type | Repayment Required? | Best For | Key Feature |

|---|---|---|---|

Grants | No | Buyers who need maximum upfront help without future debt. | It's gift money with no repayment obligation. |

Forgivable Loans | No, if you meet residency requirements. | Buyers planning to stay in the home for several years. | The loan balance gradually disappears over time. |

Deferred Loans | Yes, at the end of the loan term. | Buyers who expect future income growth or equity gain. | Repayment is postponed until you sell or refinance. |

Low-Interest Loans | Yes, with monthly payments. | Buyers who can afford a slightly higher monthly payment. | Favorable interest rates and long repayment terms. |

Understanding these distinctions is crucial. When you match your personal situation and financial goals to the right program, you can move forward with confidence and get one step closer to owning your dream home.

How to Find Down Payment Assistance Programs Near You

Knowing what down payment assistance is is one thing, but actually finding the programs available to you is the next big step. Think of it like a treasure hunt where the prize is the key to your new home. The world of these programs is incredibly local, meaning the best opportunities are often hiding right in your own community.

The assistance you can get changes dramatically from one state, county, or even city to the next. One town might offer a generous grant, while a neighboring community has a forgivable loan with totally different income limits. That's because the funding comes from all sorts of places, each with its own goals and target areas.

Start with State Housing Finance Agencies

Your first and most important stop should be your state's Housing Finance Agency (HFA). Every single state has one, and they are the central hub for homebuyer assistance. These agencies exist specifically to make housing more affordable for residents, and they manage the widest variety of DPA programs.

An HFA is your best friend for a few key reasons:

Comprehensive Listings: They lay out all the state-sponsored grants, forgivable loans, and other options in one place.

Approved Lender Lists: They’ll give you a list of mortgage lenders who are trained and certified to handle their specific DPA programs.

Official Information: You're getting the details straight from the source, so you know the eligibility rules and application steps are accurate.

To get started, just search online for "[Your State] Housing Finance Agency." Their website will be your main roadmap for seeing what's available statewide.

Explore Federal Government Resources

While most of the DPA programs you’ll use are managed locally, several federal agencies offer broader support or specific home loan programs that can shrink or even eliminate your down payment. The U.S. Department of Housing and Urban Development (HUD) is a fantastic place to begin your search.

HUD's website has a searchable database of local homebuying programs all across the country. This can help you uncover smaller, community-based initiatives you might have missed otherwise. It’s a great tool for getting a bird's-eye view of both state and local options.

Don't overlook the national resources. While most hands-on programs are local, federal sites can point you toward opportunities you didn't know existed. Your lender can help figure out how national loan programs, like FHA or VA loans, can be paired with local down payment aid to give you the biggest benefit.

The good news is that the web of support is constantly growing. As of the third quarter of 2024, there were 2,444 down payment assistance programs active nationwide, run by a mix of state agencies, cities, and nonprofits. You can read more about this growth over at the National Mortgage Professional website.

Dig into Local and Municipal Programs

This is where you can find some of the most targeted—and often most generous—assistance. Many cities, counties, and even nonprofit organizations run their own down payment assistance programs designed for the unique needs of their communities.

These hyper-local programs might be designed to:

Encourage people to buy homes in certain neighborhoods.

Support essential workers like teachers, firefighters, or healthcare professionals.

Help low-to-moderate income families put down roots.

Because these programs are so specific, they often have less competition. Check your city or county government's official website, usually under a department like "Housing and Community Development." You might find a true hidden gem.

Ultimately, your best move is to partner with a sharp mortgage lender who has real experience with DPA programs in your area. A seasoned loan officer is like a guide who already knows the terrain. They’ll know which programs are out there, which ones you’ll likely qualify for, and how to smoothly weave the DPA application into your mortgage approval, saving you a ton of time and stress.

Do You Qualify for Down Payment Assistance

This is the big question every hopeful homebuyer asks. The idea of getting thousands of dollars to help buy a home sounds amazing, but it’s natural to wonder if you’ll actually meet the requirements. The good news is that down payment assistance programs are often more flexible and accessible than people think.

Eligibility isn't about being perfect; it's about fitting within specific guidelines designed to help those who need it most. Each program has its own rulebook, but they generally revolve around a few key areas. Once you understand these common factors, you’ll have a much clearer picture of where you stand.

Decoding the Income Limits

The most common hurdle for down payment assistance is the income limit. These programs are typically aimed at low-to-moderate-income households, but you might be surprised at what "moderate income" means, especially in more expensive areas.

These limits are almost always based on the Area Median Income (AMI) for the county or city you plan to buy in. A program might say your household income can't be more than 80% or 100% of the AMI. This is simply a way to make sure the help goes to those who genuinely need a boost to compete in their local market.

It's crucial to remember this is a household income calculation—it includes the income of every adult who will be living in the home, not just the people whose names are on the mortgage.

What Is a First-Time Homebuyer

Here’s where a major myth gets busted. The term "first-time homebuyer" doesn't literally mean you've never, ever owned a home. In the world of home loans and assistance, the definition is much more forgiving.

The most widely accepted definition of a first-time homebuyer is someone who has not owned a primary residence in the previous three years. So, if you sold a home four years ago and have been renting ever since, you're back in the game.

This rule opens the door for so many people who owned a home in the past but had a life change that put them back into renting. On top of that, some programs waive this rule entirely for veterans or for buyers purchasing in specific targeted neighborhoods.

Credit Score and Property Requirements

While DPA programs are designed to be accessible, you still need to qualify for the main mortgage from a lender. That means your credit score is a big piece of the puzzle. The exact minimum score varies, but many programs align with FHA loan requirements, often looking for a score of 620 or higher.

It’s not just about you, either. The property you want to buy also has to meet a few criteria:

Primary Residence: The home has to be the place you intend to live full-time. These programs aren't for investment properties or vacation getaways.

Purchase Price Limits: Most programs set a maximum home price to ensure the assistance is used for modest, affordable housing in the area.

Property Type: Generally, single-family homes, townhouses, and condominiums are all fair game.

The Homebuyer Education Requirement

Finally, many DPA programs require you to complete a homebuyer education course. Don't look at this as just another box to check—think of it as a tool for your success. These courses are designed to get you ready for the realities of owning a home.

You'll cover essential topics like budgeting, understanding closing costs, planning for home maintenance, and avoiding foreclosure. Finishing a course not only satisfies the DPA requirement but truly equips you with the knowledge to be a confident and successful homeowner. Taking these steps can help you learn how to avoid common first-time home buyer mistakes.

When you break it down like this, the path to qualifying becomes much clearer. It’s not some exclusive club but a structured system designed to lift aspiring homeowners over that first big financial hurdle.

Here is the rewritten section, crafted to sound completely human-written and natural, following the provided style guide and examples.

Your Step-by-Step Guide to the Application Process

Let's be honest, the thought of all that paperwork is one of the scariest parts of buying a house. But applying for a down payment assistance program is way more straightforward than you probably think. It’s not some separate, nightmarish journey. Instead, it gets woven right into your main mortgage application.

Think of it like getting ready for a big road trip. You wouldn't just hop in the car and go; you’d plan your route and pack your bags first. Applying for DPA is the same idea. Each step just builds on the last, getting you closer to the closing table without any major detours.

Find a DPA-Approved Lender First

This is the most important thing you can do, so listen up: Your very first call should be to a mortgage lender who really knows the down payment assistance programs in your area.

Why is this so critical? Not every lender is approved to work with every program. Teaming up with a loan officer who doesn't know the ropes is a recipe for headaches and delays. An experienced lender is your guide. They live and breathe this stuff, so they'll pinpoint which programs you qualify for and handle both your mortgage and DPA applications at the same time. This is also the person who will get you pre-approved for your loan, which is the golden ticket that shows sellers you’re a serious buyer.

Complete Your Homebuyer Education

Once you’ve got your lender on your team and a pre-approval letter in hand, you'll likely need to complete a homebuyer education course. A lot of down payment assistance programs require this because they want to set you up for success as a homeowner for the long haul.

These aren't boring lectures. They actually cover super useful topics:

Budgeting for Homeownership: Getting a real picture of costs beyond the mortgage, like taxes, insurance, and inevitable repairs.

Managing Your Credit: Practical tips for keeping your credit score in great shape.

The Closing Process: Breaking down what actually happens when you sign all those final papers.

You can usually do these courses online at your own pace. When you're done, you’ll get a certificate of completion—hang onto that, you’ll need it for your application.

Locate an Eligible Property and Make an Offer

Now for the fun part: house hunting! Just remember that a lot of DPA programs have rules about the property itself. Your lender and real estate agent will keep you on the right track, but generally, you'll need to find a place that will be your primary home and is priced within the program's limits.

When you find the one, you’ll work with your agent to put in an offer. That pre-approval letter you got earlier? It makes your offer much stronger because it shows the seller your financing is solid.

The application for down payment assistance is almost always submitted at the same time as your main mortgage application. Your loan officer will package everything together, ensuring all the necessary forms and documents are included for both the lender and the DPA provider.

Submit Your DPA and Mortgage Applications

Once your offer is accepted, your loan officer really steps up. They'll gather up all your financial docs—pay stubs, tax returns, bank statements, and that homebuyer ed certificate—and officially submit the whole package for underwriting. This is the formal step where a professional verifies you're eligible for both the mortgage and the assistance.

It’s a single, streamlined process, not two separate ones you have to juggle. State and local programs can offer some amazing help this way. For example, some government programs offer grants or loans that are forgiven over time. New York's SONYMA program can provide a 0% interest loan that's forgiven after 10 years, and NYC's HomeFirst program can offer up to $100,000. You can dig into more of the specifics on how these state and local programs work at The Mortgage Reports.

By following these steps and leaning on your pro team, you can get through the process and unlock the funds you need to finally make that homeownership dream happen.

Common Questions About DPA Programs

As you get closer to using a down payment assistance program, it's natural for a few final questions to pop up. Home financing can feel like a complex world, but getting clear, simple answers can give you the confidence you need to take that final step toward homeownership.

Let's tackle some of the most common questions and myths floating around about DPA. We’ll clear up any lingering confusion and get you moving forward with certainty.

Do I Have to Be a First-Time Homebuyer to Qualify for Assistance?

This is one of the biggest misconceptions out there, and the answer is often a pleasant surprise: not always. While many programs are designed with first-time buyers in mind, the definition of "first-time" is incredibly flexible.

Most agencies consider you a "first-time homebuyer" if you haven't owned your primary home in the past three years. So, if you owned a house before but have been renting for a while, you might just qualify again. On top of that, plenty of programs are open to repeat buyers, especially those aimed at public service heroes like teachers, first responders, or healthcare workers.

The key is to never assume you're out of the running. Always check the specific rules for each program, because you might be a perfect fit even if this isn't your first rodeo.

Will Using a DPA Program Make My Offer Less Competitive?

This is a common fear, but it's largely a myth. In a seller's eyes, a strong offer is one backed by a pre-approved mortgage, period. It doesn't matter where your down payment funds are coming from.

The assistance is a financial arrangement between you, your lender, and the DPA provider—the seller isn't part of that conversation. When you make an offer, you'll present a pre-approval letter from your lender for the full loan amount, showing you have the financial muscle to see the purchase through.

A skilled real estate agent knows exactly how to frame your offer to highlight its strengths. They’ll focus on your solid financial pre-approval and readiness to close, making sure sellers see you as a serious, qualified buyer.

At the end of the day, a seller cares about two things: the offer price and your ability to get the financing to close on time. A DPA-backed offer checks both of those boxes just as well as any other.

Can I Combine DPA with FHA or VA Loans?

Absolutely! In fact, this is one of the most powerful ways to use down payment assistance programs. These programs are specifically built to work hand-in-hand with primary mortgages, including government-backed loans.

Here's how it often works:

With FHA Loans: FHA loans are a huge hit with first-time buyers because they only require a 3.5% down payment. Many state DPA programs are perfectly structured to cover this exact amount, making it possible to get into a home with very little cash out of pocket.

With VA Loans: VA loans are an incredible benefit for service members and veterans, often requiring no down payment at all. In this case, you can frequently use DPA funds to cover your closing costs, which can easily add up to thousands of dollars.

Your lender will be your expert guide here. They can confirm which mortgage products play nicely with your chosen DPA program and help you put together the best possible financial package. To get a better handle on these expenses, check out our first-time home buyer closing costs guide.

Does Assistance Money Need to Be Paid Back?

This is a crucial question, and the answer really depends on the type of DPA program you land. There's no one-size-fits-all answer, since assistance comes in a few different flavors.

It’s essential to understand exactly what you're being offered before you commit. Here’s a quick rundown of the main types you'll see:

Grants: This is the best-case scenario—it's gift money that never has to be repaid.

Forgivable Loans: Think of these as "silent second mortgages." The debt is forgiven over a set period, like five or ten years, as long as you live in the home. If you stay put for the full term, the loan balance just disappears.

Deferred Payment Loans: With these, you don’t make monthly payments. Instead, the full amount is due when you sell the home, refinance, or pay off your main mortgage.

Repayable Loans: These are more like traditional second mortgages. You repay the assistance over time with monthly payments, though often with a very low or even 0% interest rate.

Always ask your lender to spell out the exact terms of any down payment assistance programs you’re considering. Knowing your obligations upfront means no surprises down the road and helps you make the best choice for your future.

At RBA Home Plans, we provide award-winning architectural blueprints to help you build the home you've always envisioned. Find your perfect design by exploring our extensive online catalog at https://rbahomeplans.com.