A Guide to Second Home Mortgage Rates for Property Buyers

- Jan 10

- 17 min read

Updated: Jan 12

So, you've found the perfect getaway spot, but what about the financing? You'll quickly discover that second home mortgage rates are a different animal compared to the loan on your primary residence. Expect to see rates that are typically 0.25% to 1.0% higher.

Lenders view vacation homes as a slightly greater risk. Think about it: if you hit a financial rough patch, which mortgage payment are you going to make first? The one for the roof over your head every day, or the one for the cabin you visit on weekends? Lenders know the answer, and they price that extra risk into the loan.

How Second Home Mortgage Rates Really Work

Getting why lenders charge more for a second home is the first step toward landing a great rate. It all boils down to one word: risk.

Imagine a lender's perspective. A mortgage on your main home is their safest bet. It's where you live, and you’ll do just about anything to keep up with those payments. A second home, on the other hand, is a luxury. It's a fantastic asset to have, but it's not essential. The higher chance of a missed payment means lenders need to protect themselves, and they do that by charging a slightly higher interest rate.

The Foundation of Second Home Lending

This risk-based approach is at the very core of second home mortgages. Lenders aren't just glancing at your application; they're putting your entire financial situation under a microscope. They need to feel confident that you can juggle two housing payments without breaking a sweat, even if life throws you a curveball.

To get that confidence, they set a higher bar:

Higher Credit Scores: You might get a primary loan with a good score, but for a second home, lenders want to see an excellent one. We're usually talking 720 or higher.

Larger Down Payments: The bare minimum down payment is often 10%, but be prepared for your lender to request 20% or more to mitigate their risk.

Serious Cash Reserves: Lenders will want to see that you have enough liquid cash to cover several months of payments for both homes, just in case.

Before we dive deeper, let's examine the key differences side by side.

Primary vs. Second Home Mortgages at a Glance

This table gives you a quick snapshot of what to expect when financing your primary residence versus a vacation property.

Feature | Primary Residence Mortgage | Second Home Mortgage |

|---|---|---|

Interest Rate | Generally, the lowest available rates. | Typically 0.25% - 1.0% higher. |

Down Payment | Can be as low as 3% - 5% (FHA/Conventional). | Usually, a minimum of 10%, often 20% or more, is required. |

Credit Score | More flexible; good scores (620+) often suffice. | Stricter requirements; excellent scores (720+) preferred. |

Cash Reserves | May require 2-3 months of payments. | Often requires 6+ months of payments for both properties. |

Risk to Lender | Lower perceived risk. | Higher perceived risk due to the luxury nature. |

Occupancy | Must be your main place of living. | Must be for personal use, not primarily a rental. |

As you can see, the requirements for a second home are designed to ensure you're in a very strong financial position.

What's Happening in the Market Right Now?

The wider economy always plays a part. For instance, the mortgage world of early 2026 is an interesting place for buyers. The average 30-year fixed-rate mortgage was at 6.16% as of January 2026, a notable decrease from the 6.93% seen a year earlier. This stabilization provides buyers with a more predictable environment in which to lock in a good rate, even with the second-home premium applied.

For a real-time pulse on the market, you can always check out Freddie Mac's weekly survey data.

At the end of the day, a lender is always asking one question: "How likely are we to get our money back?" For a second home, that answer is just a little less certain, and that uncertainty shows up directly in your mortgage rate.

Securing a loan for that dream getaway is all about proving your financial rock-solid stability. If you understand the lender's perspective, you can build a stronger application and put yourself in the best position to secure the lowest possible rate.

The Key Factors That Influence Your Mortgage Rate

Think of getting a mortgage rate as a lender evaluating you. They’re looking at your whole financial picture to figure out how much of a risk you are. Strong, positive signals tell them you're a safe bet, and they'll reward you with a lower rate. Weaker signals? That means you’ll pay more.

Lenders don’t just look at one number; they're piecing together a puzzle of your financial health. Five factors really stand out. If you understand how each one works, you can put your best foot forward and lock in the best rate possible.

Your Credit Score Is King

More than anything else, your credit score dictates the interest rate you'll get. It’s a quick summary of how you’ve handled debt in the past, giving lenders a powerful clue about how you'll handle it in the future. A high score indicates reliability and instantly reduces the lender’s perceived risk.

For your primary home, a score in the high 600s might get you through the door. But for a second home, the bar is much higher. Lenders really want to see a score of 720 or higher, and a score north of 750 is your ticket to the absolute best rates on the market.

The difference isn't trivial. A borrower with a 780 credit score could easily snag a rate that’s 0.5% to 0.75% lower than someone with a 690 score for the very same loan. Over 30 years, that tiny percentage difference can translate into tens of thousands of dollars saved.

The Power of a Strong Down Payment

Your down payment is your skin in the game. From the lender’s point of view, the more money you put down, the more you have to lose. That makes you far less likely to default on the loan, which is exactly what they want to see. This lowered risk often translates directly into a better mortgage rate.

While you might be able to find a loan with a 10% down payment, most lenders strongly prefer 20% or more. Hitting that 20% mark is a huge deal for two reasons:

Lower Interest Rate: Lenders love a big down payment. A 25% down payment will almost always secure a better rate than a 10% down payment. It's a clear signal of financial strength.

Avoid Private Mortgage Insurance (PMI): On conventional loans, putting down less than 20% means you'll have to pay for PMI. This is an extra monthly fee that protects the lender—not you—and can add a hefty sum to your payment until you build up 20% equity.

Think of a larger down payment as a two-for-one deal. It reduces your loan balance and monthly payment while also showing lenders you're a low-risk borrower, earning you a more attractive interest rate.

How Lenders View Your Debt-to-Income Ratio

Your Debt-to-Income (DTI) ratio is a critical number. It simply compares your total monthly debt payments to your gross monthly income. For a second home, lenders will add your current primary mortgage payment to the new payment for the vacation home to calculate this ratio.

Lenders want to see that number below 43%, and some are even happier if it's under 40%. It proves you can comfortably juggle both housing payments without being financially stretched. A low DTI signals healthy cash flow and stability.

For instance, if all your monthly debts (including both mortgages) add up to $5,000 and your gross monthly income is $12,000, your DTI is about 41.7%. That's likely in the clear. But if that same $5,000 debt were against a $10,000 income—a 50% DTI—your application would face serious pushback or even be denied.

Choosing the Right Loan Type

The kind of loan you pick also directly affects your interest rate. For second homes, you’re almost always looking at conventional loans, since government-backed options like FHA and VA loans are only for primary residences. Even within conventional loans, you have a few choices:

Fixed-Rate Mortgages: These give you a consistent, predictable interest rate for the entire loan term, like 15 or 30 years. They are by far the most popular choice for vacation homes.

Adjustable-Rate Mortgages (ARMs): An ARM typically begins with a lower, introductory rate for a specified period (typically 5 or 7 years) before adjusting to market rates. This can be a smart move if you think you'll sell the home before the fixed period ends.

Jumbo Loans: If your loan amount is higher than the conforming loan limits set by the government, you'll need a jumbo loan. These often come with slightly higher interest rates and even stricter qualification rules due to the large amount of money involved.

The design of your future getaway can also play a role in your financing. If you're looking for inspiration, check out these inspiring house plans for vacation homes to see what’s possible.

Your Property's Intended Use Matters

Finally, what you plan to do with the property is a huge factor. Lenders put non-primary residences into two buckets: second homes and investment properties. A second home is for your personal use and enjoyment. An investment property is bought mainly to generate rental income.

Lenders see investment properties as riskier than second homes, and the loan terms show it. If your property is classified as an investment, expect higher interest rates (often 0.50% to 1.0% higher), a bigger down payment (usually 25% minimum), and tougher rules around your DTI and cash reserves. You’ll need to be crystal clear with your lender about your plans, because this one distinction will completely shape your loan.

Finding the Right Loan for Your Vacation Home

Not all mortgages are built the same, especially when you’re looking at a second property. Picking the right loan is a bit like choosing the right tool for a job—what works best depends on your finances, the home's price tag, and what you plan to do with it long-term.

When you start digging in, you'll quickly find that some of the familiar loan types aren't on the menu for vacation homes. This actually simplifies things, narrowing your focus to a few key options that lenders are comfortable with for this kind of purchase.

Conventional and Jumbo Loans: Your Go-To Options

For the vast majority of people buying a vacation home, a Conventional Loan is the way to go. These are the workhorses of the mortgage world. They aren't backed by the government, which makes them a pretty straightforward path to financing. To obtain one, you'll need a solid credit score (typically 720 or higher) and at least 10% down, although putting down 20% will likely make lenders happier.

But what if your dream cabin or beach house is located in a more expensive area? If the loan you need is bigger than the limits set by the Federal Housing Finance Agency (FHFA), you'll step into Jumbo Loan territory. These are designed for high-value properties and come with even stricter rules, often requiring higher credit scores, larger down payments (typically 20-25%), and proof of sufficient cash reserves.

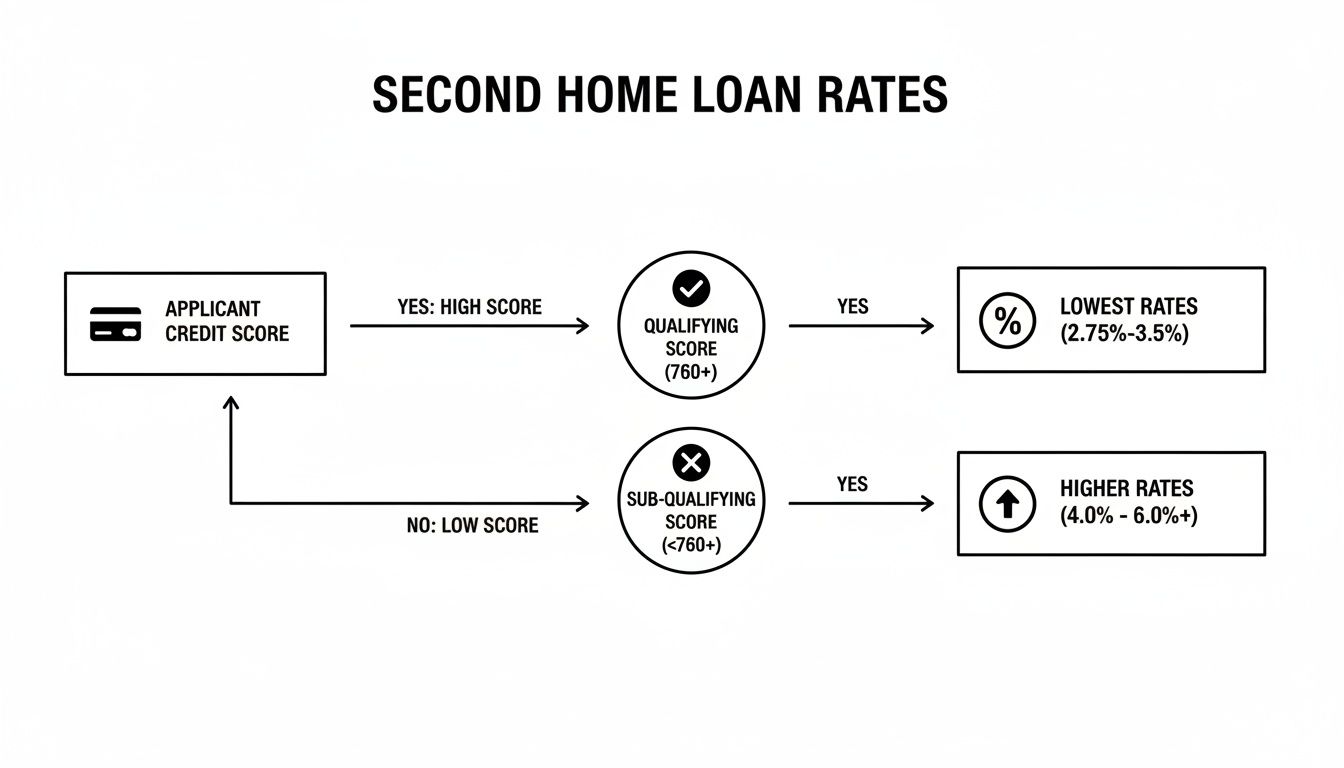

This flowchart effectively illustrates how significantly your financial health, particularly your credit score, influences the rates you’ll be offered.

As you can see, a great credit score is your first and best step toward a lower rate. It’s the clearest way lenders reward financial stability.

Why Government-Backed Loans Are Off the Table

You might have used an FHA or VA loan for your first home, and for good reason—they're fantastic programs. However, they are designed exclusively for primary residences. Their whole purpose is to help people buy the home they live in every day. Since a second home is considered a luxury, it simply doesn't meet the occupancy rules for these loan types.

This is a critical distinction that really shapes the financing landscape for vacation properties. For a deeper dive into what lenders look for, our guide on financing a second home breaks down all the requirements.

Comparing Loan Terms: 15-Year vs. 30-Year Fixed Rates

Once you've settled on a conventional or jumbo loan, your next big decision is the term. The two most common choices are the 15-year and 30-year fixed-rate mortgages. It’s a classic trade-off: do you want a lower monthly payment, or do you want to pay less interest over the long haul?

A 15-year mortgage builds your equity much faster and saves you a fortune in interest, but the monthly payment is significantly higher. A 30-year mortgage keeps your monthly payment manageable and frees up cash flow, but you'll pay a lot more in interest over the life of the loan.

Let's put some numbers to it so you can see the difference in action.

Loan Comparison Example

Feature | 30-Year Fixed Mortgage | 15-Year Fixed Mortgage |

|---|---|---|

Loan Amount | $400,000 | $400,000 |

Interest Rate | 6.5% | 5.8% |

Monthly Payment | $2,528 | $3,332 |

Total Interest Paid | $509,963 | $199,754 |

Total Savings | - | $310,209 |

Note: These are sample figures for illustrative purposes only. Your actual rates and payments will vary.

As the table shows, the 15-year option saves an incredible $310,209 in interest. But that comes at the cost of an extra $800 every month. Your decision ultimately comes down to your financial priorities: lower monthly costs now or massive savings later? If you want to see what else is out there, you can explore a wider range of global second home financing options to understand different market practices.

Choosing the right loan is all about taking a hard look at your budget and your goals. By understanding these core options, you'll be able to have a much more strategic conversation with your lender and confidently pick the loan that fits your vision.

How to Actually Qualify for a Second Home Mortgage

Getting a loan for a second home isn’t some secret art; it’s all about careful preparation. Lenders are seeking a clear and accurate picture of your financial health. Think of it like this: your application is telling them a story, and the more convincing and detailed that story is, the better your chances.

The entire process boils down to proving that you can comfortably handle two mortgage payments without any issues. To do that, you'll need to gather a complete file of your financial life, leaving no stone unturned.

Assembling Your Financial Dossier

Before a lender even glances at your application, they need to see hard proof of your income, assets, and debts. This isn't the time for ballpark figures—you need exact, verifiable documents ready to hand over. Getting this organized ahead of time will dramatically speed up the process and signal to the lender that you’re a serious, well-organized applicant.

Here’s your essential document checklist:

Proof of Income: This usually means your last two years of tax returns (both personal and business, if you have one), along with your most recent pay stubs covering a 30-day period.

Asset Statements: Lenders Want the Full Picture. You’ll need the last two months of statements for all checking, savings, and investment accounts, like your 401(k)s and brokerage funds.

Debt Information: Make a simple list of all your current debts. This includes car loans, student loans, credit card balances, and a statement for your primary mortgage.

Once you have these documents, the lender can run the single most important calculation of the whole process: your debt-to-income ratio, now with the new property factored in.

The All-Important DTI Calculation

Your Debt-to-Income (DTI) ratio is the lender’s go-to metric for gauging risk. They calculate it by adding up all your monthly debt payments—including your current primary mortgage and the proposed second home mortgage—and dividing that sum by your gross monthly income. For second homes, lenders are generally strict; they typically require a debt-to-income ratio of 43% or lower.

Let’s walk through a quick example to see it in action.

Scenario: The Mountain Cabin A family with a gross monthly income of $15,000 has their eye on a cabin. Their current primary mortgage is $2,500 per month, and they have another $1,000 in monthly debts (car payments, etc.). The new cabin mortgage, with taxes and insurance, would run $2,000 a month. * Total Monthly Debts: $2,500 (primary) + $1,000 (other) + $2,000 (cabin) = $5,500 * Calculation: $5,500 ÷ $15,000 = 0.367 * Result: Their DTI is 36.7%. That’s comfortably below the 43% ceiling, making them a very strong candidate for approval.

This calculation is a huge milestone in the journey. For a more detailed look at the entire process from start to finish, our guide on the home buying process timeline offers a great step-by-step overview.

The Crucial Role of Cash Reserves

Beyond your DTI, lenders need to see that you have a financial safety net in place. This is where cash reserves come in. These are liquid funds you have left over after paying your down payment and closing costs. For a second home, lenders often require you to have enough cash on hand to cover six months or more of payments for both properties.

This isn’t just some arbitrary box to check; it’s non-negotiable proof of stability. It assures the lender that if you hit a rough patch—like a temporary job loss—you won’t immediately default on either loan. In some cases, having strong reserves can even help offset a slightly higher DTI.

The lending market is always shifting, and broader economic trends undoubtedly play a significant role. The Mortgage Bankers Association forecasts that single-family mortgage originations will grow to $2.2 trillion in 2026. This suggests that lenders will have a greater capacity and appetite for various types of loans, including those for second homes. You can dig into the full MBA forecast on mortgage originations to see the industry outlook.

By putting together a bulletproof application with solid documentation, a low DTI, and plenty of reserves, you present yourself as the ideal, low-risk borrower that lenders are actively looking for.

Actionable Steps to Secure Your Best Possible Rate

Knowing the rules of the game is one thing; winning is another. When trying to secure the lowest possible rate on a second home, you need to be proactive. This isn't about getting lucky—it's about methodically presenting yourself as the ideal, low-risk borrower that every lender wants.

With a clear game plan, you can turn a strong financial profile into real, tangible savings. These proven steps will help you refine your application and put you in a strong position when it's time to discuss numbers.

Polish Your Credit Score Before Applying

Your credit score is the single biggest factor in the rate you’ll be offered. To a lender, a high score is proof that you’re reliable. For a second home, a "good" score just won't cut it; you really need an excellent one. Try to achieve a score above 740 if possible.

A few months before you even think about applying, start taking these steps:

Check Your Reports: Pull your credit reports from all three major bureaus—Equifax, Experian, and TransUnion. If you spot any errors, dispute them immediately.

Lower Your Balances: Focus on paying down credit card balances. High revolving debt can drag down your score, even if you never miss a payment.

Keep Payments Perfect: One late payment can do serious damage. Make sure every single bill is paid on time, without exception.

Get Past the 20% Down Payment Mark.

Your down payment is your skin in the game. While a lender might approve you with 10% down, pushing that to 20% or even 25% is a total game-changer. A bigger down payment drastically lowers the lender's risk, and they often reward you with a better interest rate.

A larger down payment does more than just lower your loan amount. It’s a powerful signal to lenders that you are financially stable and serious, often unlocking their most competitive rate tiers and helping you avoid costly private mortgage insurance (PMI).

Shop Around With Multiple Lenders

Never, ever accept the first offer you get. Mortgage rates can vary wildly between lenders, sometimes by as much as 0.50% for the exact same loan. That difference could save you tens of thousands of dollars over the life of your mortgage.

Widen your search beyond the big national banks. Get quotes from:

Local Banks and Credit Unions: These smaller institutions often have more flexible guidelines and can offer really competitive rates, especially if you already have an account with them.

Mortgage Brokers: A good broker works with dozens of lenders. They do the comparison shopping for you and can often find unique loan products that are a perfect fit.

Think About Paying for Mortgage Points

Mortgage points, also known as discount points, are essentially prepaid interest. You pay a fee upfront to the lender, and in exchange, they give you a lower interest rate for the life of the loan. Typically, one point costs 1% of the loan amount and may reduce your rate by approximately 0.25%. This can be a smart move if you know you’ll be keeping the vacation home for an extended period.

As you're getting your mortgage, it's also worth knowing that your upfront costs might offer a tax benefit. The fact that mortgage points are tax deductible can impact your overall cost of borrowing. It's always a good idea to consult with a tax professional to determine how this applies to your specific situation.

Understand and Use a Rate Lock

Mortgage rates change every single day. A rate lock is a promise from a lender to give you a specific interest rate for a set period, usually 30 to 60 days, while they process your loan.

Once you find a rate you’re happy with, ask your lender to lock it in. This move protects you from any sudden rate hikes that could happen before you close. Just be sure to ask if there are any fees for the lock and what your options are if the closing takes longer than expected. Following these steps puts you in the driver's seat of the financing process.

Common Questions About Second Home Financing

Buying a second home is exciting, but the mortgage process can raise many questions. When you’re getting ready to make an offer, you need clear, direct answers to feel good about your decisions. Let's tackle some of the most common things people ask when financing their getaway home.

Think of this as your quick guide for those "what if" scenarios. Getting these details straight can make a huge difference in your loan terms and overall financial strategy.

Can I Use Potential Rental Income to Qualify?

This is probably the most frequently asked question, and the answer comes down to one thing: how the property is classified. If you're getting a second home mortgage, the answer is almost always no. Lenders need to see that you can afford both your primary mortgage and the new one based on your current, stable income. The loan is for your personal use, so any potential rental income is just a bonus, not something they can count on.

Now, if you decide to classify the property as an investment property from the get-go, the rules change completely. In that case, lenders are much more willing to consider projected rental income. They'll usually want to see a signed lease agreement or request a detailed rental analysis from an appraiser to support the numbers.

Even then, they won’t use the full amount. Typically, lenders will only count about 75% of that projected income to offset the property's expenses, building in a cushion for vacancies and repairs. Just know that choosing the investment property route means you're looking at higher interest rates and a bigger down payment right from the start.

Second Home vs. Investment Property: What’s the Difference?

Lenders draw a very clear line in the sand between these two, and it’s critical to get it right. Misclassifying your property can stop your loan application in its tracks. It all boils down to how you plan to use the home.

A second home is a place you intend to live in for part of the year. It's for your personal enjoyment—your beach cottage, mountain cabin, or weekend condo. You have to have exclusive control over it and can't have any formal rental agreements in place when you close on the loan.

An investment property, on the other hand, is bought mainly to generate income by renting it out to others. You don't have to live there at all.

The way you classify your property is a critical fork in the road for your mortgage. A second home gets you better rates and lower down payments, but you can’t use rental income to qualify. An investment property has tougher terms but lets you use rental income to help get approved.

Here’s a simple breakdown of how lenders see them:

Feature | Second Home | Investment Property |

|---|---|---|

Primary Use | Personal enjoyment and occupancy. | To generate rental income. |

Interest Rate | Lower (typically 0.25% - 1.0% higher than primary). | Higher (often 0.50% - 1.0% above second home rates). |

Down Payment | A minimum of 10%, with 20% being common. | A minimum of 20%, with 25% or more being the standard. |

Qualifying Income | Based solely on your existing income. | Can use a portion of the projected rental income. |

IRS Rules | You must use it personally for at least 14 days per year. | No personal use requirement. |

Being completely honest with your lender about your plans isn't optional. Trying to get a second home loan for a property you intend to rent out full-time is considered mortgage fraud.

Can I Refinance a Second Home Mortgage?

Absolutely. Refinancing a second home is a common strategy that works similarly to refinancing your primary residence. You can do it to lock in a lower interest rate, change your loan term (like moving from a 30-year to a 15-year mortgage), or pull cash out of your equity.

The qualification process will feel very familiar. Lenders will take a fresh look at your credit score, DTI ratio, and the property's current value, which means you'll need a new appraisal.

There are a few great reasons to consider it:

Lower Your Rate: If market rates have dropped since you bought the place, a refinance could lower your monthly payment and save you a ton of money in interest over the life of the loan.

Tap Into Equity: A cash-out refinance lets you borrow against the equity you've built up. It's a smart way to fund a renovation, pay off other debt, or make another big investment.

Pay It Off Faster: If your income has gone up, you could refinance from a 30-year to a 15-year term. You’ll pay off the home much quicker and save a massive amount in total interest.

Be prepared for the same tough underwriting you experienced the first time. Lenders still see a second home as a riskier loan than your primary one, so you’ll need to have your finances in great shape to get the best terms.

At RBA Home Plans, we provide more than just blueprints; we offer the foundation for your dream getaway. Our award-winning designs give you the clarity and confidence to build the perfect second home. Explore our collection of vacation home plans and start your journey today!

Comments